By Monica E. Oss

Greetings from windy Clearwater Beach—and the first day of The 2024 OPEN MINDS Performance Management Institute. The day was full of discussions of every aspect related to performance—measurement, management, compensation, reimbursement, and more.

The path to performance-based provider reimbursement (and performance-based compensation) has been sporadic. Many provider organization executive teams are prepared (or preparing) for shifts to alternate reimbursement. But, particularly for specialty provider organization, the uptake has been slow—and very dependent on specific markets and specific health plans. This year, 59% of specialty provider organizations and 92% of primary are organizations are participating in some type of value-based arrangements. The majority of the arrangements are fee-for-service with performance bonuses—with 41% of specialty care and 79% of primary care organizations participating in those arrangements. These were part of the findings of our recent national survey on value-based reimbursement (VBR) and performance-based compensation, Where Are We On The Road To Value? The 2024 OPEN MINDS Performance Management Executive Survey.

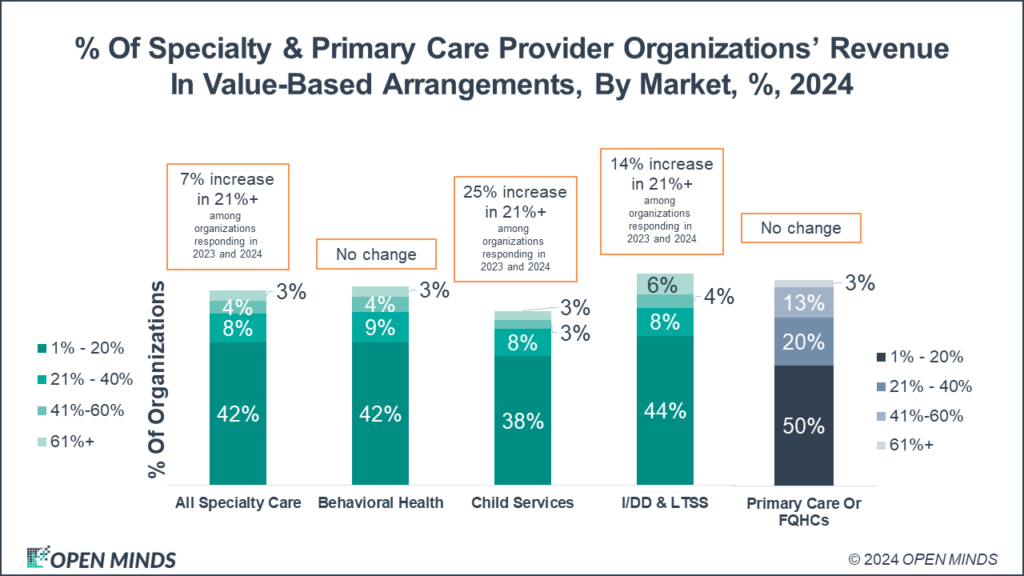

But the proportion of organizational revenue from value-based arrangements did increase year over year. For specialty care organizations, 15% of those organizations participating in value-based care have 20% or more of their revenue from those arrangements—up 7% over last year. That proportion is 36% for primary care organizations.

But as traditional provider organizations shift away from fee-for-service to some type of alternative payment arrangement, there are a new group of provider organizations (largely investor-owned) designed at the outset to accept value-based payment (largely bundled rates and case rates). Unlike traditional provider organizations that are incrementally moving from FFS to VBR, many of these risk-bearing delivery entities are designed to operate under value-based payment models from the start. This new class of provider organizations—the risk-bearing delivery entity—was the focus of a just-release report, Analyzing The Expanded Landscape Of Value-Based Entities: Implications And Opportunities Of Enablers For The CMS Innovation Center And The Broader Value Movement.

This category has a number of organizations that have become familiar names—Oak Street (now owned by CVS), Centerwell (owned by Humana), VillageMD (owned by Walgreens), and OneMedical (owned by Amazon). But there are many more—CareMax, ChenMed, Eleanor Health, CityBlock, Caremore, Concerto Care, and Cano Health. Interestingly, last week, Cano Health recently filed for bankruptcy. The operating models of these entities are not surprising—hybrid care delivery model (virtual and conveniently located in-person), multidisciplinary teams, team compensation aligned with the VBR compensation models and value-based outcomes, population health management platforms supporting clinical teams, and same day and asynchronous interface with consumers. But they pose significant competition to traditional provider organizations that are making this change. Their model—with a per-member-per-month payment for primary care and behavioral health services—is going to reshape service financing and delivery.

As these new organizations raise the bar in competition for contracts, traditional provider organization executive teams need to retrofit their operations to participate in VBR contracts. Both specialty care (29%) and primary care (39%) executive teams are finding data management and reporting to be the largest challenge to managing performance-based reimbursement arrangements. Specialty organizations are struggling to find staff who can adequately manage the contracts (18%) and build out the needed IT infrastructure (17%). Meanwhile, primary care is finding dealing the repercussions of the COVID-19 pandemic, finding experience staff to manage VBR contracts, and managing care coordination to be equally challenging (39%).

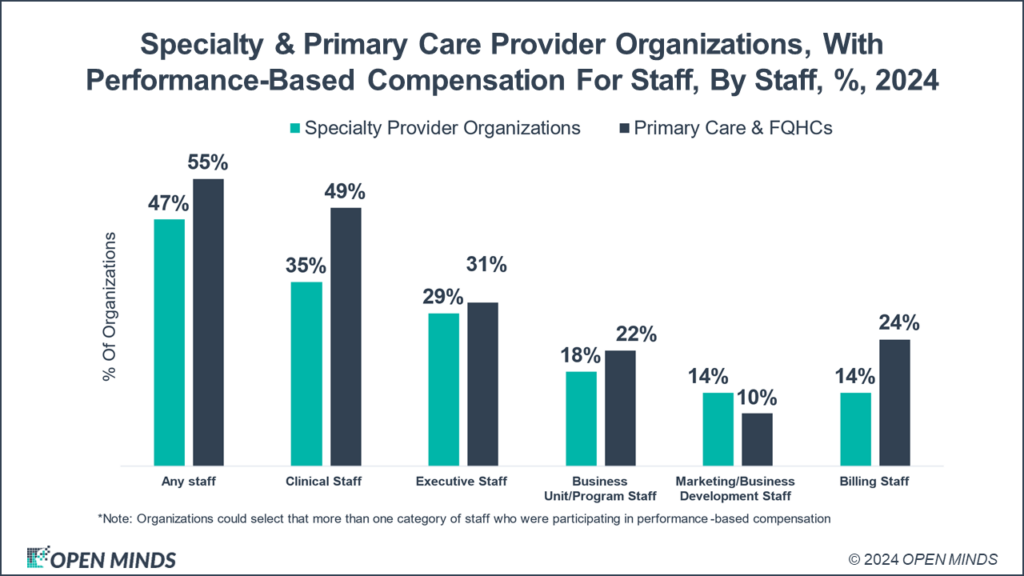

On the compensation issue, almost half of specialty provider organizations (and over half of primary care provider organizations) have performance-based compensation in place for their staff. Specialty provider organizations have performance-based measures in place for 47% of staff, 55% for primary care organizations. Most of performance-based compensation is focused on clinical staff, 35% and 49%, respectively. My surprise is how few executive teams (29% and 31%) and marketing staffs (14% and 10%) have incentives tied to performance.

While the move to value has been slow, CMS appears to be supporting the move to value-based reimbursement—and has encouraged private sector innovation and engagement. This is a continuing policy direction. Recent CMS initiatives—most notably the eight state pilot of the integrated behavioral health model and New York’s approved 1115 waiver—are new program models that will support this direction. The speed of evolution away from pay for volume may be slow, but it is steady.