By Monica E. Oss, Chief Executive Officer, OPEN MINDS

Getting your arms around the current state of risk-based, value-based, and performance-based reimbursement in the health care field is no simple task. But the recently-released market analysis—APM Measurement Progress Of Alternative Payment Models—does a good job of both definitions and measuring market movement.

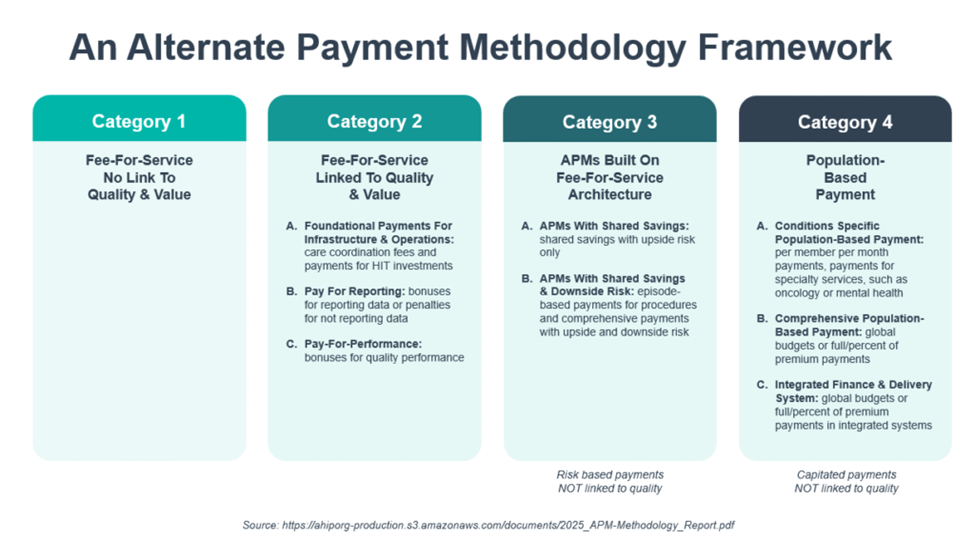

Essentially, there are four types of reimbursement—three of them grounded in traditional fee-for-service (FFS). These range from traditional volume based FFS and FFS with bonuses. There are also FFS-based alternative payment methodologies (APMs) with ‘shared savings’ and, sometimes, downside financial risk. The fourth approach is population-based payments with capitations, case rates, and other non-FFS reimbursement methodologies. The last two categories count as ‘value-based’ or ‘risk-based’ reimbursement.

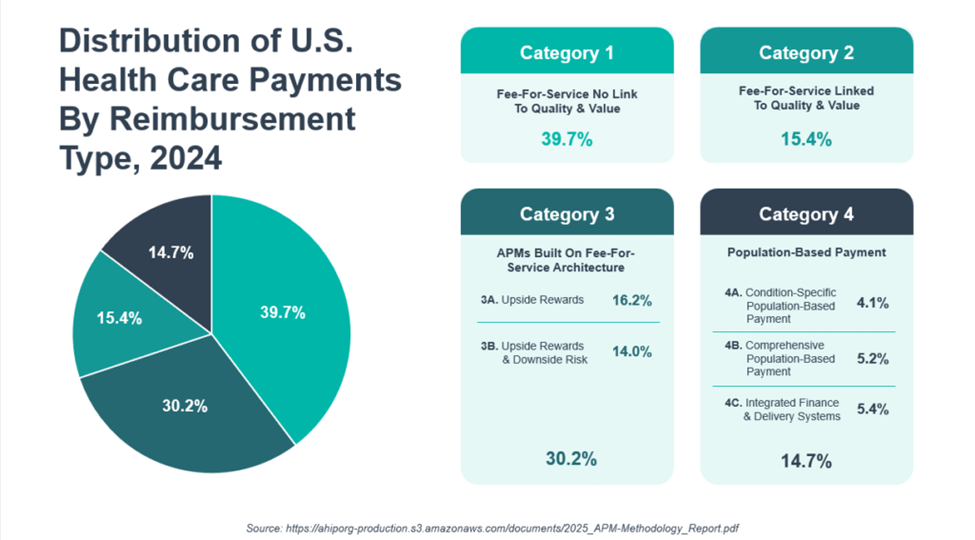

There was not a lot of year-to-year change. In 2024, 44.9% of U.S. health care payments flowed through these value-based models, compared to 45.2% in 2023. And 28.7% of health care payments flowed through APMs with downside risk, compared to 28.5% in 2023.

In commercial insurance, with 38.9% of payments in value-based models in 2024, 19.4% of payments flowed through downside risk APMs. In Medicaid, (excluding enrollees who are dually eligible for Medicare and Medicaid coverage) 42.7% of payments were in value-based models—20.6% with downside risk.

In Medicare Advantage plans, 60.0% of payments were in value-based models in 2024, 45.2% of payments flowed through downside risk APMs. And in Medicare in 2024, 44.4% of payments were in value-based models—36.4% in arrangements with downside risk arrangements.

Over the next 24 months, 70% of payer and health plan executives surveyed said they expect value-based reimbursement to increase, citing provider organization and health plan readiness as well as increasing financial pressure. In addition, 55% of executives thought that shared risk arrangements and episodic payments would grow the most.

I asked my colleague Sharon Hicks, senior associate at OPEN MINDS, about the implications of these developments for specialty provider organizations. Her observation is that the barrier to their participation in value-based reimbursement is not a single limitation, but a set of interdependent structural issues. These constraints— attribution, model and contract design, and organizational capacity—reinforce one another, creating a system-level challenge rather than a single isolated operational issue.

Attribution complexity in health plan reimbursement is a significant barrier. In many health plans, members are assigned to a specific provider of primary care—and that specific provider organization receives the capitated payment for outpatient services and shares in the savings on total cost of care. While behavioral health provider organizations provide services that frequently drive reductions in total cost, they don’t receive a share of those savings—the ‘savings’ are paid to the assigned primary care organization.

To address this reimbursement mismatch, health plans executives are shifting toward models where specialty provider organizations are also responsible for primary care for high-needs consumer. For example, Centene has introduced a behaviorally-led primary care model in the Florida market. And Optum has introduced their integrated behavioral health home model.

As Ms. Hicks explained, “It has been well documented that providing behavioral health services will assist in reducing the total medical expenditures of certain populations in their physical health spending. But the way it works is that the health plan does a value-based arrangement with a specific provider group—most often primary care. If there are savings, they are attributed to that provider group, even when behavioral health services contributed to the outcome.”

Challenges also stem from variation in contract design and performance measurement. Behavioral health organizations face a fragmented reimbursement landscape characterized by inconsistent metrics, differing risk thresholds, and variable definitions of value across Medicaid, Medicare Advantage, and commercial payers. Compounding this issue is the lack of integrated cost and outcomes infrastructure, which limits the ability to measure total cost of care and longitudinal outcomes. At the same time, there is a persistent mismatch between payer expectations for downside risk and provider capacity to assume that risk, given existing financial and data limitations.

And there is uneven readiness for reimbursement based on value across many provider organizations and health plans. Many provider organizations are limited by thin margins and financial. They also lack operational capabilities required for population health management, including care coordination systems, advanced analytics, and performance management frameworks. On the other side of the equation, health plans are handicapped by inflexible contracting models and claims payment systems, often preventing taking innovation programs to scale.

Looking ahead, specialty provider organization executive teams need a strategy to participate in whole person care models and accept value-based reimbursement arrangements with health plans. The organizations with successful strategies will have greater control of their local markets and healthier margins. As Ms. Hicks concluded, “Executive teams that can build program models that have an impact on total cost of care have significant opportunities for success in value-based models. They need to become advocates for the value of the services their organizations provide.”